VIX Term Structure as a Breakout-vs-Fade Filter

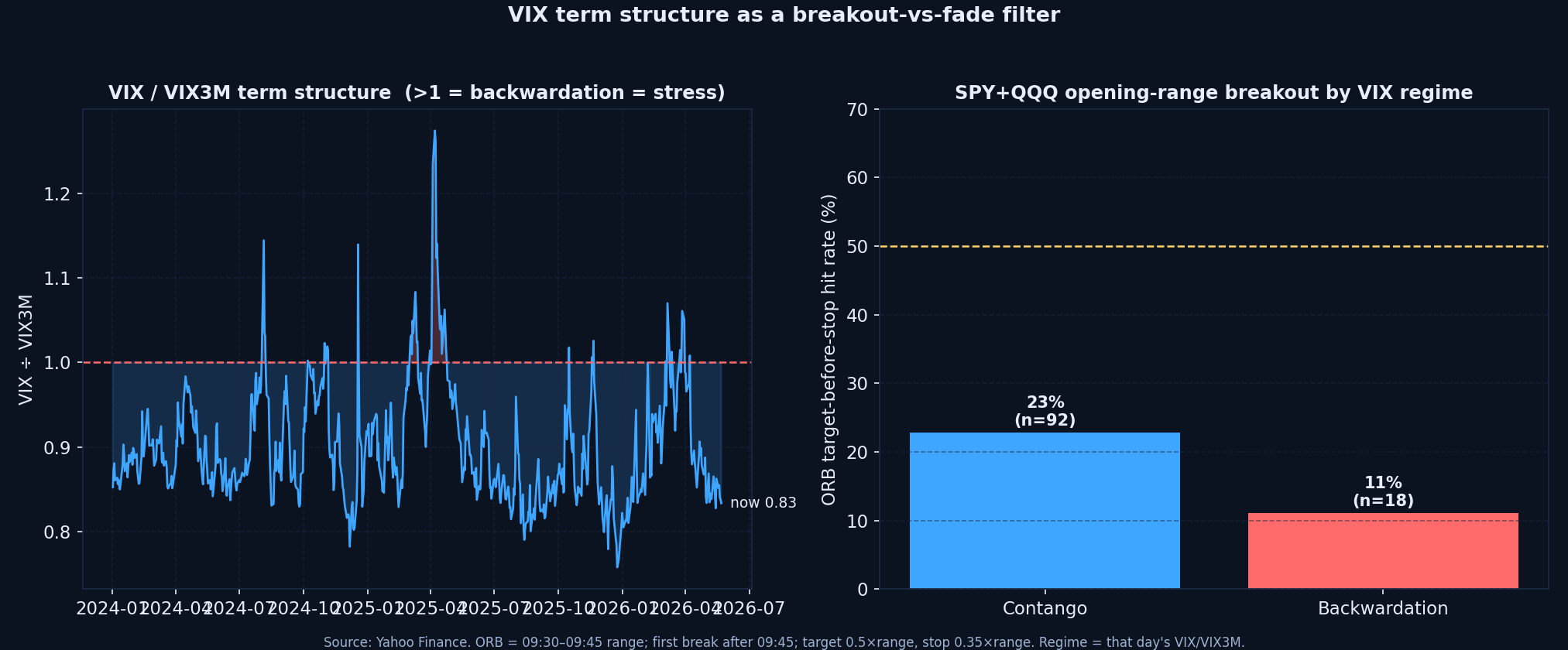

TL;DR — We split SPY+QQQ opening-range breakouts by that day's VIX/VIX3M term structure across the most recent ~50 sessions. In contango (VIX below VIX3M, the calm/dealer-long-gamma state), breakouts hit target-before-stop 23% of the time (n=92); in backwardation (VIX above VIX3M, the stress state), just 11% (n=18). Two honest conclusions: breakouts are low-probability in the current tape regardless of regime, and backwardation days are roughly twice as hostile to breakout continuation as contango days. The term structure is a useful go/slow-down filter for breakout-vs-fade — not a green light. Today's ratio sits near 0.83 (contango).

This post is a focused, measured companion to our conceptual primer, VIX Term Structure for Day Traders: When Volatility Is Fuel, Not Noise. That piece explains why the slope of the volatility curve describes the market's stress state. This one answers a narrower, testable question a day trader actually faces at 09:45: does the term-structure regime change the odds that an opening-range breakout follows through?

The test, and what it found

For each recent session we marked the 09:30–09:45 opening range, took the first break after 09:45, and scored it as a win if price reached 0.5× the range before hitting a 0.35× stop on the other side. We then tagged each day by its VIX/VIX3M ratio — below 1.0 is contango, above 1.0 is backwardation — and split the hit rate. The result:

- Contango: 23% target-before-stop (n=92). In the calm state, where front-month vol is below three-month and dealers are typically long gamma, opening breakouts followed through to a 0.5× target a bit under a quarter of the time.

- Backwardation: 11% target-before-stop (n=18). In the stress state, breakouts followed through roughly half as often. Backwardation days are sharp-reversal days: the opening break is more likely to be a sweep that gets faded than a trend that pays.

- Both are below 50% — by design and by regime. A 0.5× target against a 0.35× stop is a demanding, positive-reward structure, so a sub-50% hit rate can still be profitable. But the current tape is not a breakout-friendly regime, and the term structure tells you which days are least friendly of all.

The honest framing: the term structure does not turn breakouts into a high-probability trade. It tells you when to demand more confirmation and when to favor the fade. Contango ≈ breakouts are merely difficult; backwardation ≈ breakouts are a trap and the reversal is the higher-quality setup.

Why the slope predicts breakout quality

The mechanism is the dealer gamma regime that sits underneath the term-structure slope. When front-month vol is below longer-dated vol (contango), the options complex is usually net long gamma and dealer hedging is stabilizing — it dampens moves and lets an established break grind toward a measured target. When the front end inverts above the back (backwardation), hedging flips destabilizing and price action becomes whippy: opening breaks overshoot, then snap back through the range as the move that triggered the break also triggers the hedging that reverses it. That is the structural reason backwardation breakouts fail more often, and it's the same gamma logic behind VIX-Implied Exhaustion Walls.

How to use it at 09:45

- Check the ratio before the bell. VIX/VIX3M under 1.0: breakouts are tradeable with normal confirmation. Over 1.0: tighten the checklist, cut size, and give the fade equal billing. It pairs directly with VIX-Adjusted Opening-Range Sizing.

- In backwardation, flip the default. When the curve is inverted, the higher-probability trade is fading the failed opening break back into the range, not chasing the breakout. The 11% breakout hit rate is the other side of a strong fade.

- Confirmation matters more in stress. VWAP acceptance, basket agreement (QQQ/SPY) and real flow — not just a print through the level — are non-negotiable on backwardation days. The 09:30–09:45 Auction study and the ORB statistical framework cover the confirmation stack.

- Routing follows the regime. Backwardation days run wider spreads and faster reversals; route choice and risk-off awareness matter more. See Risk-Off Routing.

What this is not

This is not a claim that contango breakouts are easy — 23% is still a sub-coin-flip hit rate that only works because the reward exceeds the risk. It is also a recent-regime measurement: the backwardation sample is small (n=18) because inverted days have been rare, and the relationship should be re-measured as conditions change. The durable takeaway is directional and mechanical: the volatility term structure conditions breakout follow-through, contango is friendlier than backwardation, and the inverted-curve day is a fade day until proven otherwise.

Related reads

VIX Term Structure for Day Traders · VIX-Adjusted Opening-Range Sizing · The 09:30–09:45 Auction · VIX-Implied Exhaustion Walls · Risk-Off Routing.

Join the desk

If you already condition your breakout-vs-fade decision on the volatility regime — and can show the data behind it — that's the standard our platform is built around. The trader application takes about ten minutes; serious applicants receive a response within five business days.

#VIX #TermStructure #Contango #Backwardation #OpeningRangeBreakout #ORB #Gamma #DayTrading #RegimeFilter #PropTrading #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade