Hard-to-Borrow Mechanics: The Hidden Cost Layer in Short Selling

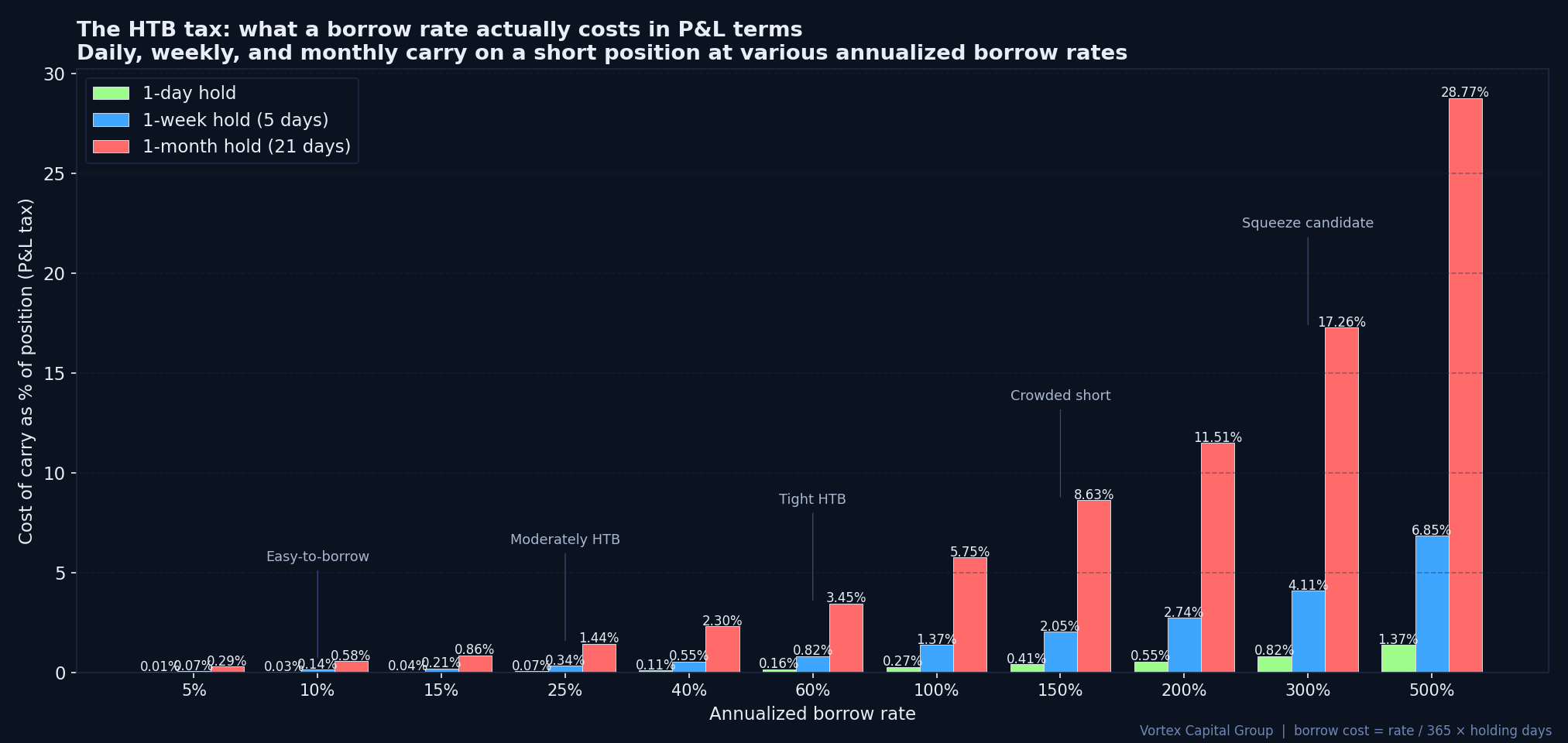

TL;DR — Hard-to-borrow short selling is an infrastructure problem dressed up as a trade idea. A 100% annualized borrow rate is a 0.27%/day P&L tax. Over a 5-day hold that's 1.37%, and on a 21-day hold it's 5.75% — often the entire expected alpha of the trade. We treat locate availability, borrow rate, term-borrow security, and recall risk as part of the trade decision, not a separate operational concern. The chart, the route, and the borrow desk are one workflow.

Short selling looks straightforward in the chart. The level fails, the seller takes the trade. The reality lives in a parallel infrastructure most traders rarely have to think about. Shares have to be located before they can be sold. The locate has an availability state, a quoted rate, a term structure, and a recall risk. None of those variables appear on the chart, and all of them decide whether the trade actually exists.

Long traders can afford to read execution as a secondary concern — wide-distribution liquidity, smart routing, and a routine relationship with one venue carry most setups acceptably. Short traders cannot. The infrastructure is the trade for any name with non-trivial borrow stress, and treating it as separate is the textbook way to leak edge across an entire year.

What a borrow rate actually costs you

Read the chart line by line and the math is clear:

- Easy-to-borrow (1–5% annualized): negligible day-trade cost. Less than 1.4 bp per day. The borrow rate isn't part of the trade decision; the setup is.

- Moderately HTB (10–25%): 3–7 bp per day. Still tradeable on multi-day swings, but the rate eats into smaller-edge setups. A 20-bp expected alpha on a 5-day hold pays away 15–30% of expected return.

- Tight HTB (40–60%): 11–16 bp per day. The trade only makes sense with high-conviction directional alpha and short holding periods.

- Crowded short (100–150%): 27–41 bp per day. Day trades only. A two-day hold burns 55–80 bp — close to the expected alpha on most short setups.

- Squeeze candidate (200%+): 55 bp+ per day. The rate itself is a signal that the borrow desk has run out of supply. Trading these names short on a multi-day hold is fighting both the directional risk and a near-1% daily carry tax.

The four moving parts of an HTB short

1. Locate availability. Before sending the short, the broker must locate borrowable shares. For easy-to-borrow names, the locate is automatic and pre-cleared. For HTB names, the locate has to be requested, often with limited supply. If 100 traders are pre-marketing the same short, the first 30 get filled, the next 50 wait, and the last 20 don't get filled at all. Time of request matters; we've seen names where the entire desk's available supply gets allocated within 90 seconds of the borrow desk opening.

2. Borrow rate. The annualized cost to hold the short. Quoted by the lender, accruing daily, charged against the position. Rates can reprice intraday on hot names — a 50% morning rate can become 200% by the close if demand spikes. We see this most often in pre-earnings windows and after surprise corporate developments.

3. Term borrow vs. open borrow. Open borrow can be recalled by the lender at any time. Term borrow locks in supply for a fixed period (commonly 1, 5, or 30 days) at a negotiated rate. Term protects against recall but doesn't protect against rate hikes if the term ends mid-position. Choosing between them is part of the trade plan — if the thesis is multi-day and the name is high-recall-risk, paying up for term is part of the cost.

4. Recall risk. When a lender requires their shares back, the broker has to either find replacement shares or close the short via a buy-in. Buy-ins happen at the market price, often during the worst possible moment — when the short is already against the trader. A recalled position can be force-closed in minutes; we've watched it happen on names where the borrow desk warned 60 minutes in advance and others where there was no warning at all.

Reg SHO threshold names

The SEC's Regulation SHO maintains a daily "threshold securities list" — names where fail-to-deliver levels have exceeded specified thresholds. These names carry tighter close-out requirements, more aggressive recall enforcement, and structurally higher borrow rates. Reading the threshold list is part of pre-market preparation; the names there have repeatedly demonstrated the failure modes the rule was designed to address.

Practical implication: a name appearing on the Reg SHO list for several consecutive sessions is a name where the short side has been crowded enough that the standard market mechanisms are struggling. The borrow rate may be quoted at 30%, but the realized cost — including the probability of mid-trade recall and emergency buy-in — is materially higher. We size accordingly.

The desk decision tree

- Idea acceptable AND easy-to-borrow → execute normally. Locate is automatic, rate is negligible, recall risk is zero. Treat as a standard short.

- Idea acceptable AND moderate HTB (10–40%) → execute, but size for the borrow tax. Holding period must be short enough that the carry doesn't dominate expected alpha.

- Idea acceptable AND tight HTB (>40%) → secure locate first, term borrow if multi-day. If locate is unavailable, the trade isn't real — no amount of chart conviction overrides supply.

- Idea acceptable AND squeeze candidate (>150%) → we require a same-day exit plan, defined buy-in tolerance, and pre-defined position size cap. The trade is now a tactical short, not a thesis short.

- Idea acceptable BUT locate unavailable → the trade doesn't exist for us today. Move on. Forcing it via marginal lenders or alternate vendors is where most retail-style HTB blow-ups originate.

Where vendor redundancy earns its keep

A single HTB vendor is a single point of failure. When one vendor's supply runs dry on a name, another vendor may still have shares. When one vendor reprices a name to 200% mid-session, another may still be at 80%. When one vendor recalls, another may have term. Our desk maintains four-vendor HTB coverage precisely because the cost of being shut out of a setup by one vendor's supply state is materially higher than the cost of running four relationships. The full operational case is in our four-HTB-vendors piece.

How borrow connects to the rest of execution

Short selling exposes weak execution stacks faster than long selling. A bad fill on a long entry hurts; a bad fill on a short entry can be followed by a buy-in that hurts much more. The borrow desk's status at 09:30 affects every short setup our scanner ranks at 09:25. The route choice on the short execution affects whether the position telegraphs intent to the borrow desk before fill (which can trigger an immediate rate hike). We covered the wider execution model in our DMA vs retail broker piece — short-side specifically depends on every layer of that model holding together simultaneously.

Joining the desk

Vortex Capital Group supports qualified short-biased traders with four-vendor HTB locate access, multi-clearing redundancy, DMA execution through Sterling Trader Pro, and the order-flow tooling needed to time entries before borrow tightens. We want applicants who can describe their borrow workflow as cleanly as their chart workflow — when they request locates, when they take term, how they size into rate uncertainty, what their recall response looks like. The trader application takes about ten minutes; every serious candidate is reviewed personally.

#HardToBorrow #HTB #ShortSelling #BorrowRate #RegSHO #Locates #DayTrading #PropTrading #DMA #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade