OPG Orders & the Opening-Print Edge: ETF iNAV Dislocations

TL;DR — Most traders react to the opening print; a few supply it. The OPG (at-the-opening) order participates only in the opening auction and cancels if unfilled — which is exactly what you want when a thinly traded ETF's first trade has drifted away from the fair value (iNAV) of the basket it holds. You compute fair value before the bell, post a buy/sell OPG limit at fair-value-minus-your-edge, take only the mispriced fill, hedge the basket, and exit on convergence minutes later. The edge is the fill, not a market view — and it is real but thin, competitive, and unforgiving of a sloppy fair-value model.

Most traders treat the opening print as a price to react to. A small number treat it as a price to supply — and they do it with an order type most retail platforms bury three menus deep: the OPG, or “at-the-opening” order. An OPG participates only in the opening auction and cancels if it does not execute there. You get the opening print or nothing. For a particular, narrow situation — an illiquid ETF whose first trade has drifted away from the fair value of what it holds — that “opening print or nothing” property is exactly the point.

What an OPG order actually is

An OPG order is a market or limit order flagged to participate solely in the primary listing exchange’s opening cross (the NYSE or Nasdaq opening auction). It does not rest on the book during the continuous session. If it is not filled in the cross, it is cancelled. That is a feature, not a limitation: it lets a desk express a view that is only valid at the single moment when the auction sets one clearing price for an accumulated imbalance of overnight orders — and walk away cleanly if the print does not come to them.

The companion order types matter too. A LOC (limit-on-close) and MOC (market-on-close) do the same job for the closing auction; an OPG limit lets you cap the price you will accept in the opening cross. The strategy below lives or dies on using the limit variant: you are not trying to trade the open, you are trying to trade the open only if it prints away from fair value.

Where the dislocation comes from

Every ETF has an intraday fair value — the iNAV, or indicative NAV — equal to the live value of its underlying basket. For a liquid fund like SPY, authorized participants and high-frequency market makers keep the traded price welded to that basket within a basis point or two; there is nothing to do. The opportunity is structural and it lives in the thinly traded names: narrow sector funds, single-country and emerging-market equity ETFs, niche fixed-income funds.

Two things conspire in those names. First, the opening book is shallow, so the auction clears a small imbalance against a stale resting price. Second — and this is the larger effect — the underlying basket has often moved overnight while the ETF’s last print did not. A Japan or EM equity ETF closed at 4:00 PM ET on yesterday’s basket marks; by this morning’s US open, the constituents (or their proxies and futures) have repriced on overnight news. If the opening cross prints close to yesterday’s level while the basket’s fair value has moved 1–2%, the first trade is mechanically rich or cheap to iNAV. The desk that has computed iNAV before the bell knows which, and by how much.

A worked example

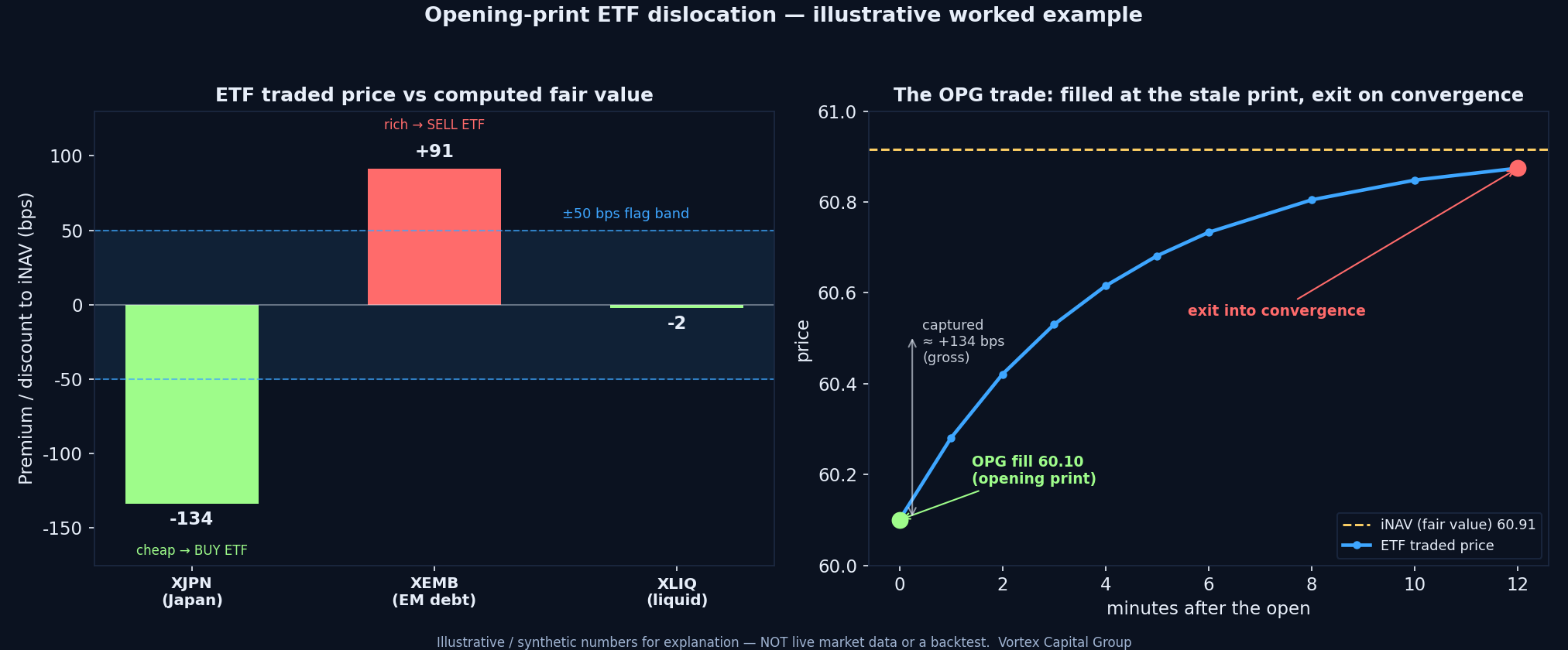

The numbers below are an illustrative worked example — synthetic, chosen to show the mechanism cleanly, not a live trade or a backtest. Take a thinly traded Japan equity ETF, “XJPN,” that struck a published NAV of 60.00 at yesterday’s close. Overnight, the Nikkei constituents it holds rallied; pricing the basket leg-by-leg against current quotes (and futures/FX for the names whose home market is shut) puts this morning’s fair value — the iNAV — at 60.92, up about 1.53%. But XJPN is illiquid, and its opening cross clears at 60.10 against stale resting orders. That is a discount of roughly −134 basis points to fair value: the ETF is cheap to what it holds.

The left panel is what a fair-value scanner surfaces before the bell: XJPN cheap by 134 bps (buy candidate), a hypothetical EM-debt fund “XEMB” rich by 91 bps (sell candidate), and a liquid control “XLIQ” sitting at −2 bps — inside any sane flag band and therefore ignored. The right panel is the trade: a buy OPG limit gets filled at the 60.10 print, and as the continuous session begins and the ETF’s price is dragged back toward the basket it represents, the position is exited into that convergence. The captured move is the gap to iNAV, gross of costs.

The phrase the desk uses is that the fill is the edge. You are not predicting market direction. You post a limit at fair-value-minus-your-required-edge and accept only fills that are already mispriced relative to a value you computed. Then you close shortly after, as the print converges — often within minutes. The risk you are left holding between fill and exit is basket risk, which is why the clean version of the trade is hedged immediately against index futures, a liquid proxy ETF, or the basket itself.

What this is not

This is not free money, and the honest version of the post has to say why. The wide quoted spreads on these ETFs exist precisely because the resident market makers price adverse selection into them — they know the overnight gap is there too. The cleanest form of the trade belongs to authorized participants, who can create and redeem shares at NAV and collapse the premium directly; without AP status you are running a convergence stat-arb and bearing inventory risk until it converges, which is not guaranteed to happen by your exit.

The edge is also thin and competitive. In any ETF with meaningful assets, the dislocation is arbitraged away in the cross itself. What is left is genuinely neglected, low-AUM funds where the imbalance is too small for the large players to bother — which is the same reason your own size is capped. And computing iNAV faster and more accurately than the auction is the entire game: for funds whose underlying market is closed overnight, you are modelling fair value off futures and FX proxies, and a sloppy model produces confidently wrong signals. A −134 bps “edge” that is really a −30 bps stale-proxy error is a losing trade.

How Vortex traders run it

Fair value before the bell. The desk computes iNAV for a watchlist of thin ETFs ahead of the open, pricing each basket leg-by-leg — with futures and FX proxies for constituents whose home market is shut — and ranks names by premium/discount. The candidate list is the handful that breach a flag threshold set to round-trip cost plus the required edge, not merely non-zero. A dislocation inside that band is noise, and Vortex Edge filters it out before it ever reaches a trader’s screen.

The order type is the strategy. This is a pure execution play, and it is not expressible on a retail platform that only offers market and limit orders in the continuous session. DMA through Sterling Trader Pro gives the desk native OPG and LOC order types routed directly to the primary listing exchange’s auction — the difference between participating in the opening cross at a price you control and chasing the first continuous print after the imbalance has already cleared. The same routing discipline we covered in DMA vs retail broker execution is not a nicety here; it is the whole trade.

Hedge the basket, not the view. Because the position carries basket risk between fill and convergence, it is hedged on fill against futures or a liquid proxy. The P&L target is the spread to iNAV, isolated from where the broad market goes in the next ten minutes.

Exit on convergence, not on hope. The trade has a defined thesis — the print was stale, the continuous session will drag it to fair value — and a defined invalidation. If convergence does not begin, the thesis is wrong and the position comes off; it is not allowed to become a directional bet on a name you only ever wanted to arb.

It belongs to the same family as the auction work we have published on the opening range and the closing auction magnet: the auction is a distinct liquidity event with its own mechanics, and the edge is in understanding the order types that let you participate in it on your terms.

Bottom line

The opening-print ETF trade is a clean illustration of a Vortex principle: a real edge is usually an execution edge, not a prediction. You compute what a thing is worth, you let the auction offer you a price, and you act only when the print is demonstrably wrong — using an order type built for exactly that moment. The view is trivial. The fair-value model, the routing, and the discipline to take only mispriced fills are the hard part, and they are where the money is.

Further reading

DMA vs retail broker execution · The 09:30–09:45 auction: opening range breaks that pay · The closing auction magnet · The PFOF tax.

Join us

If you already think in terms of fair value versus the print — and you can say exactly how each order is routed and why — that is the standard our platform is built around. The trader application takes about ten minutes; serious applicants hear back within five business days.

#OPGorders #OpeningAuction #ETFArbitrage #iNAV #MarketMicrostructure #Execution #DMA #OpeningCross #PropTrading #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade