MSTR & COIN as Intraday Bitcoin Beta: Sizing the 2.5× Proxy

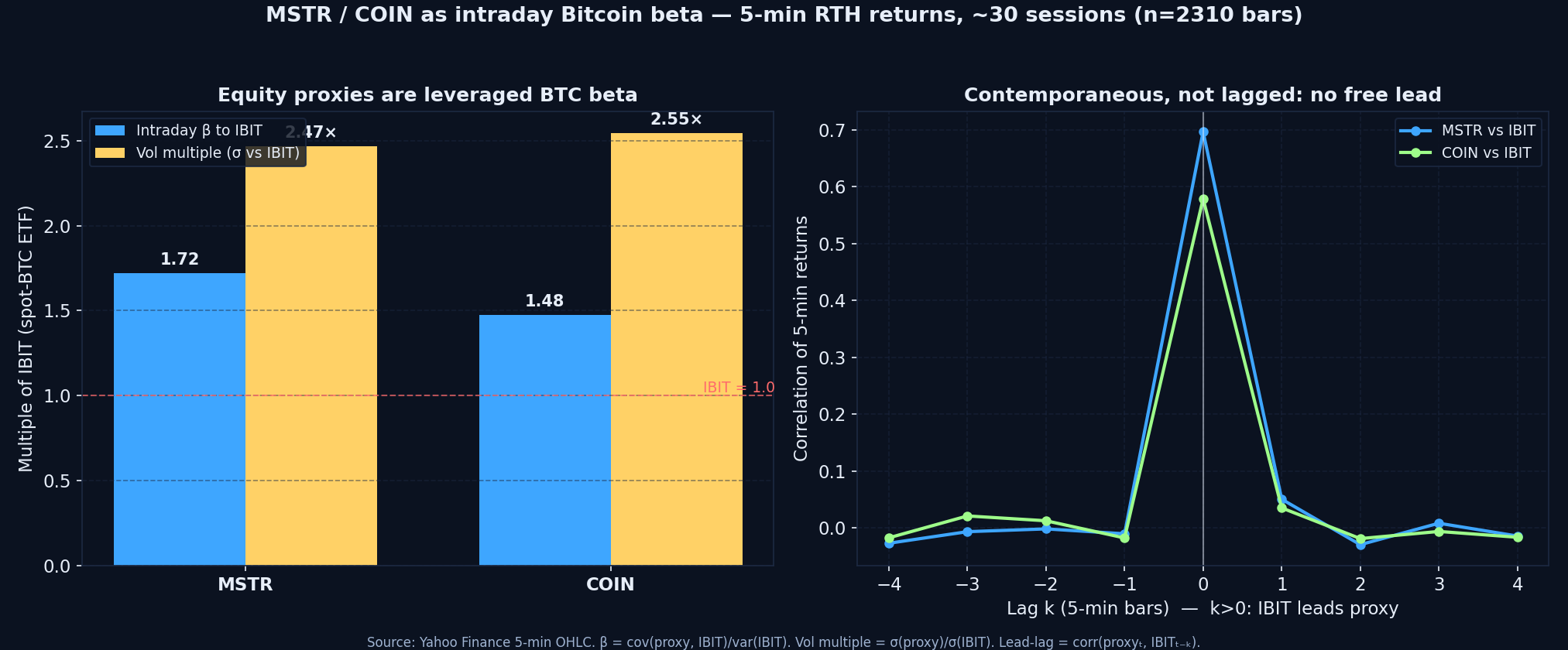

TL;DR — Over ~30 recent sessions of 5-minute regular-hours data (n=2,310 bars), MSTR carried an intraday beta of 1.72 to IBIT (the spot-BTC ETF) and 2.47× its realized volatility; COIN ran 1.48 beta and 2.55× vol. The relationship is contemporaneous — cross-correlation peaks at lag 0, so neither IBIT nor the equity proxy reliably leads the other on a 5-minute clock. The trade is not "watch BTC, then buy MSTR." The trade is: size MSTR and COIN as ~2.5× leveraged crypto exposure with single-name idiosyncratic risk bolted on, and respect that the leverage cuts both ways inside the same bar.

"MSTR is just leveraged Bitcoin" is half true, and the wrong half is the expensive one. For a day trader the useful questions are quantitative: how much does the equity proxy move per unit of spot move, is that relationship stable enough to trade intraday, and does anything lead anything? We measured it directly rather than relying on the narrative.

What the 5-minute tape actually shows

We pulled 5-minute regular-session bars for MSTR, COIN and IBIT across roughly the last 30 trading days, stripped the overnight gap from each session's first bar, and computed intraday log-return statistics against IBIT as the spot-BTC reference. Three results matter for execution:

- Beta is well above 1, but below the headline leverage. MSTR's intraday beta to IBIT was 1.72 and COIN's was 1.48. The often-quoted "5× Bitcoin" framing describes balance-sheet and option-implied leverage over weeks, not the bar-to-bar cash-equity response a day trader is actually exposed to.

- Volatility multiple is the number to size on. MSTR realized 2.47× and COIN 2.55× the per-bar volatility of IBIT. Same-dollar position in MSTR is roughly two-and-a-half times the intraday risk of the same dollars in the ETF. That is the figure that belongs in your share-size math, not the beta.

- There is no free lead. The cross-correlation of 5-minute returns peaks sharply at lag 0 and decays to noise within one or two bars in either direction. IBIT does not telegraph MSTR, and MSTR does not telegraph IBIT, on this timeframe. Anyone selling a "BTC leads the proxy by X minutes" intraday signal is fitting noise.

Why beta and vol-multiple disagree — and why vol-multiple wins

Beta blends correlation and relative volatility. The equity proxies are noisier than IBIT — earnings, ATM issuance, premium-to-NAV swings, index flows — so a chunk of their variance is idiosyncratic and uncorrelated with spot. That pulls beta down even while the raw volatility multiple stays above 2.4×. For sizing, the volatility multiple is the honest input: it captures the full intraday range you are exposed to, including the single-name risk that beta launders out.

Practical translation: if your risk unit is calibrated to a normal IBIT day, cut MSTR and COIN share size to roughly 40% of what the price ratio alone would suggest, then check it against the live spread. The proxy will give you a normal-looking entry and an abnormal-looking stop-out distance.

Where the proxy decouples from spot

Contemporaneous correlation does not mean the proxies are pure BTC tracks. The decoupling windows are exactly where day-trade P&L is made and lost:

- Equity-specific catalysts. MSTR issuance announcements, convertible activity and premium-to-NAV repricing can move the stock while spot is flat. COIN trades on exchange volume, regulatory headlines and its own earnings. On those bars, beta to IBIT temporarily collapses.

- Session boundaries. Bitcoin trades 24/7; the equity proxies do not. The overnight spot move is compressed into the equity's opening print, which is why we excluded the first bar of each session — and why the pre-market read matters. See The Pre-Market Echo.

- Borrow and the short side. Shorting MSTR or COIN intraday is a different animal from shorting an ETF. Borrow can tighten fast on a high-beta name in a selloff. A short thesis without a confirmed locate is not a trade — see Hard-to-Borrow Mechanics.

How the desk trades it

We treat MSTR and COIN as leveraged crypto-beta vehicles with an idiosyncratic overlay, not as Bitcoin substitutes. That means three rules. First, size on the volatility multiple, not the price or the beta. Second, use IBIT (or BTC) as a regime confirmation, not an entry trigger — because there is no lead, the confirmation has to be contemporaneous flow, which is where reading Level 2 and CVD on the proxy itself earn their keep. Third, route deliberately: these names run wide spreads on volatile bars, and a few basis points of slippage compound hard against a 2.5×-vol instrument. The PFOF Tax math is unforgiving here.

The volatility regime also matters. High-beta crypto proxies behave very differently when the broader vol term structure flips — the same logic we apply in VIX Term Structure for Day Traders and the Yield-Shock Playbook.

Related reads

Hard-to-Borrow Mechanics · Reading Level 2 Like a Prop Trader · The PFOF Tax · DMA vs Retail Broker Execution · VIX Term Structure for Day Traders.

Join the desk

If you size on realized risk rather than headline leverage, and you can explain how you'd route a 2.5×-vol name without donating the edge, that's the standard our platform is built for. The trader application takes about ten minutes; serious applicants receive a response within five business days.

#MSTR #COIN #IBIT #Bitcoin #BTCproxy #DayTrading #Volatility #PositionSizing #OrderFlow #PropTrading #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade